Unless you’ve been hiding under a rock, you’ve probably gathered that I’m a massive fan of Monzo.

I’ve signed up to their waiting list for a current account (position 15,880), I’m an avid follower of them on socials and in general tech media and I had a bit of a fan-girl moment last week when I got to listen to one of its founders, @hugocornejo, talk about building the business around listening to what people want at Canvas 2017.

Why, you ask? It’s simple - they have created not only an aesthetically beautiful product (I literally can’t wait to pay for things using my coral debit card or see emoji flash up when I get a spending notification) but they have created a product that actually solves customer issues and poor experiences, combining user insights and clever touches to help people become more responsible with their money and truly visualise their spending habits.

Traditional banking companies have been talking for years about responsible lending and why you should save, but they didn’t do anything other than make it harder for people to access services when they really needed it.

Monzo is leading a revolution and I like it. So this got me thinking - if they've achieved the impossible in a firmly traditional sector such as banking, what would happen if they did housing? Well, I reckon it would look something like this….

They would focus on problem solving, not creating things they ‘think’ people want.

We tend to make a lot of assumptions in the housing sector. OK, we do have things like Universal Credit and Welfare Reform to contend with, but how many companies can honestly say they took into account customer needs and problems when thinking about their service delivery models as opposed to how their Board and Executive Team thought their services should be offered?

Problem definition is really important here, as you need to know that what you are planning to do solves an actual issue, not create a set of smaller ones - Monzo would do this at the very beginning of any new ideas, and if its not going to solve anything, they'd move onto the next one.

They would offer a fully mobile solution that harnesses instant, in app payment technologies and social media platforms so customers can engage how they want, through which medium they want, when they want.

The day of the contact centre is dead - I mean, how annoyed do you get when, god forbid, you actually have to talk to somebody to solve a problem! Instead, colleagues that have traditionally held these roles would be up-skilled to assist customers via web chat and social media. It's still a personal service, just one that has moved into the 21st Century. I hate to say it, but we have also got to get round the notion of offering contact between the hours of 9am-5pm.

In a world where people are working shifts, across geographical boundaries and everything is connected 24/7, why do we force our customers to accept such draconian hours when you or I wouldn't?

They would use clever ways to deploy positive nudge theory.

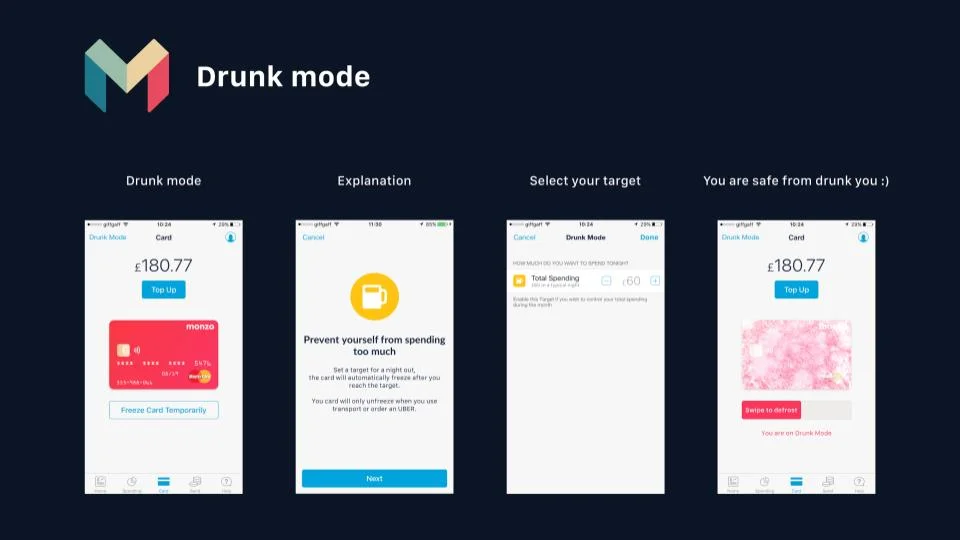

Now, I’m not suggesting you introduce something like Monzo’s ‘Drunk Mode’ (where customers can tell the app to set a spending limit before a night out, and once that point is reached, your card is frozen so you can’t go over it), but an ability to nudge customers to make the right decisions or take on additional responsibility in relation to their tenancies? Something as simple as giving a customer control over their own affairs can pay dividends in the long run, we just need to provide them with basic tools to do it.

Housing associations have spent so long being paternalistic and enforcing, customers have only ever really heard from us when something has gone wrong. We’d get better value for money from our resources if we deployed them to engage and encourage customers.

They would use systems that collect meaningful data on behaviours and send fun, informative reports to customers to allow them to make lifestyle or behavioural changes.

We sit on a lot of useful data but the traditional housing legacy systems don’t always make it a) easy to access or b) present it in a format that’s useful. Knowledge is power, so if we deployed basic data science principles and provided easy to digest, personalised summaries, we can help support customers in the best possible way. HA’s can benefit from meaningful data too by using information on customer behaviours to inform their future service designs. Whoever says you can't predict the future has clearly never met a data scientist.

They would utilise a community of customers to suggest new developments or service features and also ask for constant feedback that is actually used.

I’m going to say it - I’m not talking about the usual group of volunteers that come along because you are providing free cake, coffee and transport. In order to get a proper representation of your customers, you need to make sure the feedback group make up accurately reflects this. It’s no good people under 30 having the majority on a panel looking at residential care for over 60’s, likewise it's no good for over 50 males giving feedback on young women's services. Rocket science it is not, but more than this, it's important to actually act upon the feedback you are given.

Monzo have a thriving customer community, that has voted on items from new product additions or enhancements to the way Monzo charges customers when they go overseas and guess what - they have adopted every single winning suggestion.

They would use small, agile teams to deploy the service offering, focusing on stuff they are good at.

Business 101 tells you that big, unwieldy hierarchical structures are hard to manage and lead to inefficiencies and silo working, and to its credit, the sector is pretty good at avoiding this. Monzo would go one step further though and focus on what it's good at, choosing to invest time, money and resources into activities that support that vision. Great at Tenancy Support but rubbish at doing repairs? Team up with someone who can do that for you. Famous for your communities work but your housing management functions could do with a shake up? Form a working group with others in the area.

Ultimately, stop being a jack of all trades when it might actually be at a detriment to your business and customers.

Lastly, and possibly most importantly, they would be completely transparent.

Literally, everything would be out there for customers to access if they want it. Customer trust and loyalty is the most important currency they can transact with and this is the same no matter what industry you are in.

Now, I’m not advocating you rip up your business plans or get rid of contact centres - we have to contend with many internal and external factors that often dictate how we operate, particularly if public money is being used. What I am suggesting is that we should channel our inner 'Monzo' in that just because it’s different (or dare I say it, revolutionary), it doesn’t mean that we shouldn’t try. As a sector, we are embracing innovation like never before, with the creation of groups and role profiles in this area of expertise (*coughs loudly*), and it is paying dividends. I’m confident that if Monzo can achieve all of this positive disruption within banking, we as a sector can follow their example and start doing something similar within housing.

In the meantime, if you need me, I’ll be sat here patiently waiting for my account…..